At Quest Loans we are committed to obtaining the best loan programs and pricing for everyone from first time home buyers to experienced investors. Let us do the all legwork when it comes to researching the various loan programs available in today’s market. If you are looking to refinance or purchase a new property, let Quest Loans provide you with the Best Rates, Best Service, Period.

Contact us at 1-888-883-5252 to get started on your loan! Or you can email us at information@questloans.com if you have any questions!

Showing posts with label loans. Show all posts

Showing posts with label loans. Show all posts

Thursday

Sunday

Is it possible to "buy" a better rate?

Even if you're unsure of how long you plan to keep your mortgage before you move or refinance, paying points now for a lower rate may make sense. For example, do you have a high-paying job now but you think you might change careers in the next few years? We can help you sort it out. It's part of our goal to find you the right loan for your means and future.

A point -- which equals one percent (1%) of the total loan amount -- is an up-front fee that lowers your annual interest rate and total interest due over the life of your loan. So, a one point loan will have a lower interest rate than a no point loan. Basically, when you pay points you trade off paying money later in favor of paying money now. You can pay fractions of points, meaning there are a lot of points packages that can make a loan's terms more favorable if that's what's right for you.

There are a variety of rate and point combinations available. When you look at different loan programs, don't look just at the rate -- compare the whole package. Federal law requires lenders to publish their loans' Annual Percentage Rate, or A.P.R. The A.P.R. is a tool used to compare different terms, offered rates, and points.

Monday

Fannie Mae vs Freddie Mac: What is the difference?

You may hear the names Fannie Mae and Freddie Mac often. But what are they exactly?

They are both Government Sponsored Enterprises (GSE) in the home mortgage business. They are very similar. they both buy mortgages on the secondary market, pool them, and then sell them as mortgage-backed securities to investors in the open market. The way they handle government guarantees, subsidies and direct government funding are the same.

Their main difference is that Fannie Mae primarily buys mortgages issued by banks while Freddie Mac buys mortgages issued by thrifts.

Fannie Mae was a federal program that was created in 1938 as part of the New Deal, and Freddie Mac was chartered by Congress as a private corporation in 1970. Fannie was monopolizing the mortgage market as a government agency until it became a private corporation in 1968. Freddie Mac was brought into the market to compete with Fannie Mae's monopoly so that lenders and bankers would have two options instead of just one. Today, Fannie Mae is a privately-owned corporation while Freddie Mae is a stockholder-owned corporation.

Fannie Mae allows guarantee on multiple properties owned by a single person up to 10 units, while Freddie Mac allows guarantee on no more than 4 units. They do have a slight difference in rules regarding down payments as well. Fannie Mae asks as little as 3% from home loan borrowers and Freddie Mac requires at least a 5% down payment, which means that it does not allow loans of more than 95% loan-to-value.

They both have a common goal in mind: to provide affordability to homeowners. They aim to provide a stability to the mortgage market so that it can continue to function. While Fannie and Freddie compete with each other in the same market, they really are very similar and have the same basic foundation and goals to help you, as a homeowner, get the most affordable loan that you can. Ask your loan officer what is best for you.

They are both Government Sponsored Enterprises (GSE) in the home mortgage business. They are very similar. they both buy mortgages on the secondary market, pool them, and then sell them as mortgage-backed securities to investors in the open market. The way they handle government guarantees, subsidies and direct government funding are the same.

Their main difference is that Fannie Mae primarily buys mortgages issued by banks while Freddie Mac buys mortgages issued by thrifts.

Fannie Mae was a federal program that was created in 1938 as part of the New Deal, and Freddie Mac was chartered by Congress as a private corporation in 1970. Fannie was monopolizing the mortgage market as a government agency until it became a private corporation in 1968. Freddie Mac was brought into the market to compete with Fannie Mae's monopoly so that lenders and bankers would have two options instead of just one. Today, Fannie Mae is a privately-owned corporation while Freddie Mae is a stockholder-owned corporation.

Fannie Mae allows guarantee on multiple properties owned by a single person up to 10 units, while Freddie Mac allows guarantee on no more than 4 units. They do have a slight difference in rules regarding down payments as well. Fannie Mae asks as little as 3% from home loan borrowers and Freddie Mac requires at least a 5% down payment, which means that it does not allow loans of more than 95% loan-to-value.

They both have a common goal in mind: to provide affordability to homeowners. They aim to provide a stability to the mortgage market so that it can continue to function. While Fannie and Freddie compete with each other in the same market, they really are very similar and have the same basic foundation and goals to help you, as a homeowner, get the most affordable loan that you can. Ask your loan officer what is best for you.

Tuesday

Are you pre-qualified or pre-approved for a loan?

To get pre-qualified for a loan, I will collect information about your debt, income, and assets. We’ll look at your credit profile and assess goals for a down payment and get an idea of different loan programs that would work for you. I will issue you a pre-qualification letter indicating the amount you are pre-qualified to borrow.

It is important to understand that a pre-qualification letter is just an estimate of what you are eligible to borrow, not a commitment to lend. Getting pre-approved for a loan gives you competitive advantage when the time comes to bid on a home because you have been approved for a loan for a specified amount.

To get pre-approved, you will complete a mortgage application and provide me with various information verifying your employment, assets and financial status such as W-2 forms, bank records and credit card statements. We’ll review your mortgage options and submit your application to the lender that best meets your needs. Once the application process is complete you will receive a pre-approval letter indicating the amount your lender is willing to lend you for your home.

A pre-approval letter is not binding on the lender; it is subject to an appraisal of the home you wish to purchase and certain other conditions. If your financial situation changes (e.g. you lose your job), interest rates rise or a specified expiration date passes, your lender must review your situation and recalculate your mortgage amount accordingly.

Sunday

Veteran Affairs (VA) Loans

Other benefits of a VA loan include:

Negotiable interest rate.

Closing costs comparable – and sometimes lower - than other financing types.

No private mortgage insurance requirement.

Right to prepay loan without penalties

Mortgage can be taken over (or “assumed”) by the buyer when a home is sold.

Counseling and assistance available to veteran borrowers having financial difficulty or facing default on their loan.

Although mortgage insurance is not required, the VA charges a funding fee to issue a guarantee to a lender against borrower default on a mortgage. The fee may be paid in cash by the buyer or seller, or it may be financed in the loan amount.

A VA loan can be used to buy a home, build a home and even improve a home with energy-saving features such as solar or heating/cooling systems, water heaters, insulation, weather-stripping/ caulking, storm windows/doors or other energy efficient improvements approved by the lender and VA.

Veterans can apply for a VA loan with any mortgage lender that participates in the VA home loan program. A Certificate of Eligibility from the VA must be presented to the lender to qualify for the loan.

Saturday

Closing Costs: What is included?

Loan-Related Closing Costs

Loan Origination Fee

This covers the administrative expenses in setting-up and processing the loan. The loan origination fee may be a percentage of the mortgage amount.

Points (optional)

An option for the home buyer is to pay points to lower the interest rate at which the loan will be repaid. Each point equals 1 percent of the mortgage amount. For example: on a $150,000 loan, 1 point would equal $1,500.

Appraisal Fee

The fee for having the house appraised may be incorporated into the closing costs or payment may be required by the lender at the time the loan application is submitted.

Credit Report

The lender uses a credit report to determine the creditworthiness of the loan applicant. This fee is often paid when the loan application is submitted.

Interest Payment

Typically the buyer is required to pay interest on the mortgage loan to cover the time between the closing date and when the first mortgage payment period begins. For example: If closing is on May 15. Your first monthly payment begins to accrue interest on June 1 with your first mortgage payment due July 1. At closing an interest payment covering the accrual period between May 15 and May 31 may be required.

Escrow Account

At closing a payment may be required to fund the escrow account if the lender is paying home insurance, property taxes and/or other expenses out of the escrow account.

Insurance Closing Costs

Homeowner's Insurance

This insurance covers replacement costs for damages caused by fire, wind or other disaster that might affect the value of the property. Typically, the insurance also includes personal liability and theft coverage.

Flood or Quake Insurance

Additional hazard insurance coverage that is required for homes located in a designated hazard zone as established by the Federal Emergency Management Agency (FEMA). An appraiser, inspector, or your realtor can let you know if a property resides in a hazard zone.

Private Mortgage Insurance (PMI)

Insurance required for conventional mortgage loans when the borrower's down payment on the house is less than 20 percent of the loan value.

Title Insurance

This policy protects both the buyer and lender by insuring a clear chain of title. (In other words, it insures that that the person who sells the house has the legal right to do so.)

Loan Origination Fee

This covers the administrative expenses in setting-up and processing the loan. The loan origination fee may be a percentage of the mortgage amount.

Points (optional)

An option for the home buyer is to pay points to lower the interest rate at which the loan will be repaid. Each point equals 1 percent of the mortgage amount. For example: on a $150,000 loan, 1 point would equal $1,500.

Appraisal Fee

The fee for having the house appraised may be incorporated into the closing costs or payment may be required by the lender at the time the loan application is submitted.

Credit Report

The lender uses a credit report to determine the creditworthiness of the loan applicant. This fee is often paid when the loan application is submitted.

Interest Payment

Typically the buyer is required to pay interest on the mortgage loan to cover the time between the closing date and when the first mortgage payment period begins. For example: If closing is on May 15. Your first monthly payment begins to accrue interest on June 1 with your first mortgage payment due July 1. At closing an interest payment covering the accrual period between May 15 and May 31 may be required.

Escrow Account

At closing a payment may be required to fund the escrow account if the lender is paying home insurance, property taxes and/or other expenses out of the escrow account.

Insurance Closing Costs

Homeowner's Insurance

This insurance covers replacement costs for damages caused by fire, wind or other disaster that might affect the value of the property. Typically, the insurance also includes personal liability and theft coverage.

Flood or Quake Insurance

Additional hazard insurance coverage that is required for homes located in a designated hazard zone as established by the Federal Emergency Management Agency (FEMA). An appraiser, inspector, or your realtor can let you know if a property resides in a hazard zone.

Private Mortgage Insurance (PMI)

Insurance required for conventional mortgage loans when the borrower's down payment on the house is less than 20 percent of the loan value.

Title Insurance

This policy protects both the buyer and lender by insuring a clear chain of title. (In other words, it insures that that the person who sells the house has the legal right to do so.)

Wednesday

Understanding the Terms: "APR" and "Interest Rate"

You'll see an interest rate and an Annual Percentage Rate (A.P.R.) for each mortgage loan you see advertised. The easy answer to "why" is that federal law requires the lender to tell you both.

The A.P.R. is a tool for comparing different loans, which will include different interest rates but also different points and other terms. The A.P.R. is designed to represent the "true cost of a loan" to the borrower, expressed in the form of a yearly rate. This way, lenders can't "hide" fees and upfront costs behind low advertised rates.

While it's designed to make it easier to compare loans, it's sometimes confusing because the A.P.R. includes some, but not all, of the various fees and insurance premiums that accompany a mortgage. And since the federal law that requires lenders to disclose the A.P.R. does not clearly define what goes into the calculation, A.P.R.s can vary from lender to lender and loan to loan.

The A.P.R. on a loan tied to a market index, like a 5/1 ARM (adjustable mortgage rate), assumes the market index will never change. But ARMs were invented because the market index changes and makes fixed rate loans cheaper or more expensive to make -- that's why they're variable rate in the first placed!

So, A.P.R.s are at best inexact. The lesson is that A.P.R. can be a guide, but you need a mortgage professional to help you find the truly best loan for you.

Note when you're browsing for loan terms that the A.P.R. will not tell you about balloon payments or prepayment penalties, or how long your rate is locked. Also, you'll see that A.P.R.s on 15-year loans will carry a higher relative rate due to the fact that points are amortized over a shorter period of time

The A.P.R. is a tool for comparing different loans, which will include different interest rates but also different points and other terms. The A.P.R. is designed to represent the "true cost of a loan" to the borrower, expressed in the form of a yearly rate. This way, lenders can't "hide" fees and upfront costs behind low advertised rates.

While it's designed to make it easier to compare loans, it's sometimes confusing because the A.P.R. includes some, but not all, of the various fees and insurance premiums that accompany a mortgage. And since the federal law that requires lenders to disclose the A.P.R. does not clearly define what goes into the calculation, A.P.R.s can vary from lender to lender and loan to loan.

The A.P.R. on a loan tied to a market index, like a 5/1 ARM (adjustable mortgage rate), assumes the market index will never change. But ARMs were invented because the market index changes and makes fixed rate loans cheaper or more expensive to make -- that's why they're variable rate in the first placed!

So, A.P.R.s are at best inexact. The lesson is that A.P.R. can be a guide, but you need a mortgage professional to help you find the truly best loan for you.

Note when you're browsing for loan terms that the A.P.R. will not tell you about balloon payments or prepayment penalties, or how long your rate is locked. Also, you'll see that A.P.R.s on 15-year loans will carry a higher relative rate due to the fact that points are amortized over a shorter period of time

Monday

Definitions of Common Mortgage Terms

One issue commonly arises when first time home buyers begin their mortgage application process: understanding the definitions of various mortgage terms. If you are not familiar with the process or the industry, there is plenty of jargon that could slow down this process for you. We want you to fully understand these terms and how they apply to you and your future new home.

Definitions

Annual income

Your annual income before taxes. For married couples this is your total combined annual income before taxes.

Purchase price

The price of the home you wish to purchase. This is the actual price you'll pay, not including any closing costs.

Total monthly payment

Total monthly payment that you can qualify for. This is the total of principal, interest, taxes and insurance paid each month. Often called PITI.

Cash on hand

Cash you have for the down payment and all closing costs.

Interest rate

The current annual interest rate you can receive on your mortgage.

Definitions

Annual income

Your annual income before taxes. For married couples this is your total combined annual income before taxes.

Purchase price

The price of the home you wish to purchase. This is the actual price you'll pay, not including any closing costs.

Total monthly payment

Total monthly payment that you can qualify for. This is the total of principal, interest, taxes and insurance paid each month. Often called PITI.

Cash on hand

Cash you have for the down payment and all closing costs.

Interest rate

The current annual interest rate you can receive on your mortgage.

Friday

Reminders for Home-buyers

It is important to understand your personal financial situation before getting a mortgage. The amount of money a banker is willing to lend you might not be how much you can afford to borrow.

Make sure to learn the loan jargon before you start mortgage-shopping. It will make everything that much easier!

When choosing the best type of fixed-rate or adjustable-rate, decide how long you want to keep the loan and how much financial risk you can accept.

A good way to get the loan you want is to craft a positive and truthful mortgage application, just as you would prepare your resume to get the job you want.

If you already own a home, refinancing could save you money! Stay up to date with the current interest rates!

If you would like more information on getting your own mortgage application started, contact Felix Katz of Quest Loans at 805-456-1201. He would be happy to answer any questions you may have.

Make sure to learn the loan jargon before you start mortgage-shopping. It will make everything that much easier!

When choosing the best type of fixed-rate or adjustable-rate, decide how long you want to keep the loan and how much financial risk you can accept.

A good way to get the loan you want is to craft a positive and truthful mortgage application, just as you would prepare your resume to get the job you want.

If you already own a home, refinancing could save you money! Stay up to date with the current interest rates!

If you would like more information on getting your own mortgage application started, contact Felix Katz of Quest Loans at 805-456-1201. He would be happy to answer any questions you may have.

Wednesday

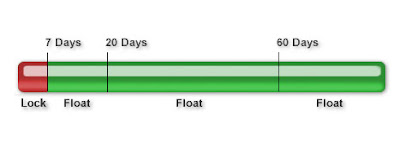

Understanding the Terms: "Lock" and "Float"

If I were considering financing or refinancing a home today, I would do the following: Lock if my closing was taking place within 7 days or Float if my closing was taking place between 8 and 60 days from now.

This is only my opinion of what I would do if I were financing a home. It is only an opinion and cannot be guaranteed to be in the best interest of all/any other borrowers. Brought to you by the professionals at Quest Loans.

Basically, a deposit is paid by a borrower to lock in an interest rate for a specific period of time while a mortgage application is being processed. If interest rates decline during this period, the float down option allows the borrower to obtain a lower rate.

For example, suppose a borrower locks in a rate of 5%. Before the borrower's mortgage application is complete, however, interest rates drop to 3.5%. If this borrower has a mortgage rate lock float down, they may lock in the lower mortgage rate before the mortgage is approved.

This is only my opinion of what I would do if I were financing a home. It is only an opinion and cannot be guaranteed to be in the best interest of all/any other borrowers. Brought to you by the professionals at Quest Loans.

What does this mean?

For example, suppose a borrower locks in a rate of 5%. Before the borrower's mortgage application is complete, however, interest rates drop to 3.5%. If this borrower has a mortgage rate lock float down, they may lock in the lower mortgage rate before the mortgage is approved.

Monday

Welcome!

Welcome to 411 Rates, the place to get all the info you need about mortgages in a way you can understand it. We know that applying for a mortgage can be a daunting task. There is so much to know and the jargon can really make it confusing. Don't worry, you have come to the right place!

We would like to help you break down the entire loan process so that you aren't left scratching your head while you sign your name. It is important to know what you are agreeing to and how it will effect your life.

Please bookmark us and continue checking back for our frequent simple but informational posts regarding mortgages.

We would like to help you break down the entire loan process so that you aren't left scratching your head while you sign your name. It is important to know what you are agreeing to and how it will effect your life.

Please bookmark us and continue checking back for our frequent simple but informational posts regarding mortgages.

Subscribe to:

Posts (Atom)